Risk & Diversification Audit

There was a prominent note released last week from Savita Subramanian strategists that noted “too many red flags” and ultimately advised to “take profits.” Although taking profits is not my reaction to the data, nor my preferred strategy, I am nervous about this moment for many of the same reasons. Here are some analytical concerns and then some things to consider.

Macroeconomic Risk

We are starting to see some of the high volatility normally associated with inflationary growth. These environments can produce some of the most exceptional and disappointing stock market returns.

Uncertainty around a potential Fed hiking cycle has spooked markets since last Friday. This fear is warranted, considering the high inflation and strong jobs numbers released in the past month.

Valuation Risk

The S&P 500 notched an all time low in shareholder yields last week.

Valuations are strongly correlated with drawdowns during a recession. Any hiccup in the economy or markets risks a ~50% correction (see the linked letter for this valuation-based estimate). This is a good framework for detached investors to confirm their risk tolerance.

Everything is AI

Not only are SpaceX, Anthropic, and OpenAI likely coming public this year, public hyperscalers are now selling equity and debt at scale. This dilutes already low yields for existing investors.

Normally, businesses invest in capex after seeing growth in the economy. This datacenter spending carries heavy ROI uncertainty because it has preceded macroeconomic growth.

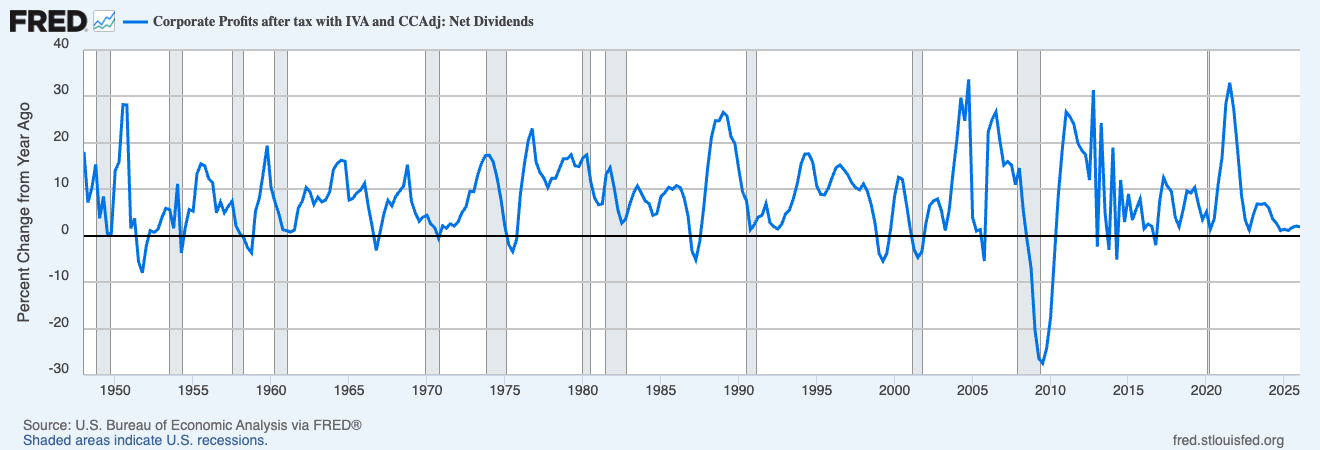

Despite record-breaking earnings growth, shareholder payments were only up 1.9% in Q1 2026. So far, almost all earnings are being reinvested back into capex and the AI theme instead of benefiting shareholders. AI ROI is still unknown.

Index Diversification

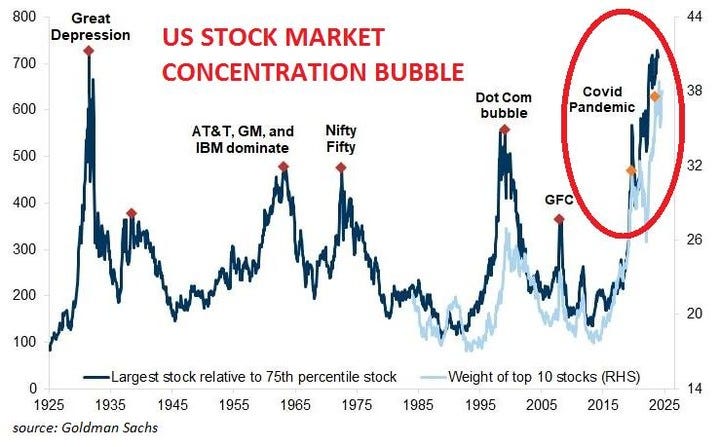

The largest 10 stocks in the index now make up > 40% of the S&P 500. This is potentially the most concentrated market in the last 100 years.

This would be fine, if not for the strong correlation of ideas among the top 9 stocks. I suspect that 8 of 9 companies are heavily dependent on AI ROI.

Low quality companies, measured by Fama-French via trailing volatility, are getting far more attention than high quality companies. This dynamic makes it hard to stick to prudent investment strategies, but provides an opportunity to diversify away from the index and into high quality investments.

Signs of Capital Rotation

Value investing is doing well for investors this year, and providing some level of protection/diversification. Most value indices are beating the S&P 500 year over year and year to date.

The MAG7 is struggling under the weight of its capex requirements and IPO competition. We can see this dynamic played out in its year to date underperformance of international stocks (VXUS), small-caps (IWM), and value stocks (IWD) as of June 10.

Conclusion

I think the “take profits” advice is too short-sighted and behaviorally dangerous. Investors sitting in cash won’t feel great if this market continues to rip. There will likely be quite a bit of FOMO on the way up before there is any comfort on the way down. Even Stan Druckenmiller, one of the greatest investors of our time, couldn’t resist that FOMO during the internet bubble.

https://novelinvestor.com/stan-druckenmillers-worst-mistake-ever/

That said, there are probably many investors who have stumbled into more risk than their goals or appetite would prescribe. Now is a good time to confirm that your asset allocation aligns with your financial plan and risk appetite.

Something closer to my north star of investing is to always demand sufficient diversification. My biggest concern from this analysis is that the broad market indices are no longer diverse. If your portfolio has drifted into a heavy market-weighted index allocation over the last few years, now is an excellent time to audit your actual exposure.

Disclosures & Risk Information: The views expressed in this commentary are for informational and educational purposes only and represent the current macroeconomic opinions of the author as of June 2026. This material does not constitute personalized investment advice, a legal opinion, or an endorsement, recommendation, or solicitation to buy or sell any specific security or adopt any specific investment strategy. Sector, index, or ETF performance mentioned (including VXUS, IWM, and IWD) is historical, represents gross-of-fees data, and does not guarantee future results. All indices are unmanaged and cannot be invested in directly. Diversification does not ensure a profit or protect against loss in a declining market. Past performance is no guarantee of future results.