The Growth War

And Finding Value Havens

There’s a school of thought, one that I subscribe to, that the best way to invest is to buy quality companies at a discount. This style of investing is often referred to as “Value” investing. Some of the oldest and best research on equities measured value and published on its efficacy.

In part because value investing recently endured its worst decade in history, value investors have nearly gone extinct.

This new year is recycling old styles however, and value stocks are back on the menu. The Value ETF $VTV is up 8.2% year to date while the S&P 500 is only up 0.3%. The original P/B value factor is now outperforming the S&P 500 over the past 10 years.

Value investing is the tip of a much larger and more visceral AI story. AI represents innovation, it represents growth, and it represents disruption.

Economic growth is a threat to incumbents. AI threatens to topple longstanding near-monopolies. One industry at the front lines of intensifying innovation is the software sector, which is down -23.1% year to date. Incumbents do not find growth friendly and the S&P 500 is chalked full of tech incumbents with a lot to lose.

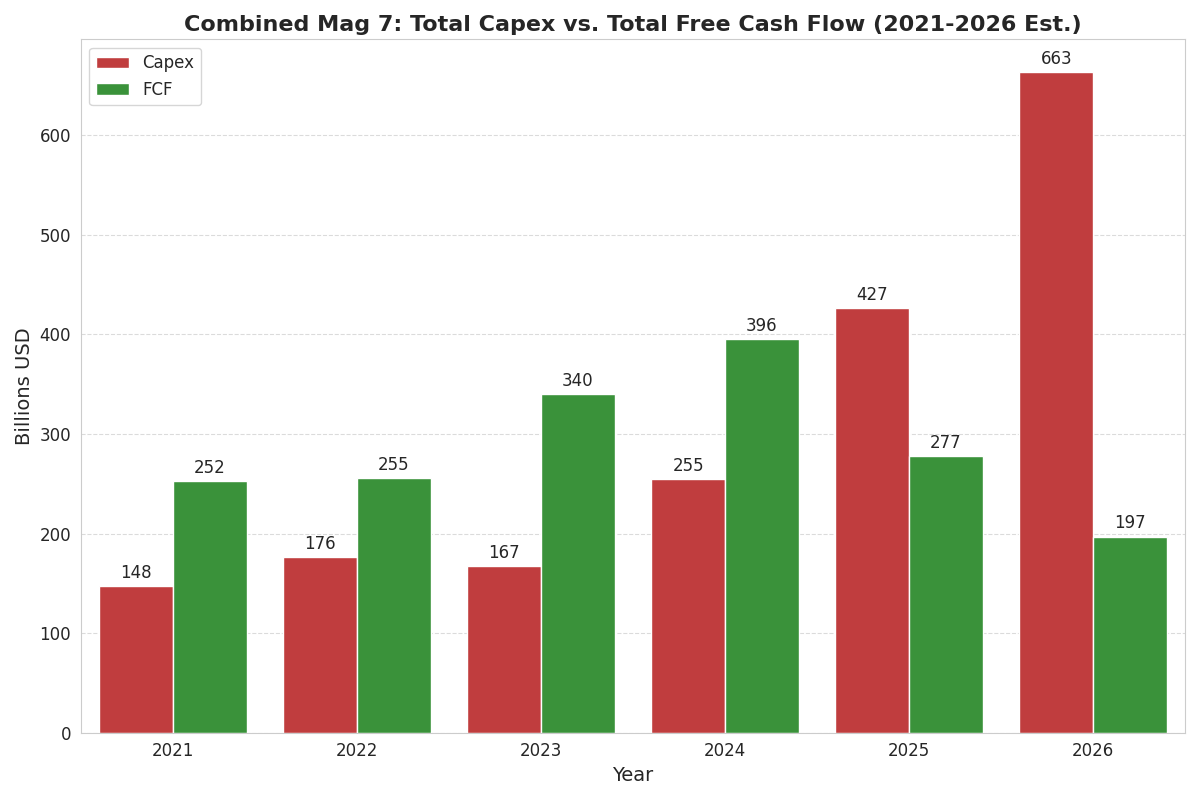

Even the hyperscalers, the companies commanding AI investment, are bleeding from the battle. The Mag 7 returned $396B of free cash flows to shareholders in 2024 but projections have those free cash flows reduced to $197B in 2026. Some companies have reduced their free cash flows to zero and are starting to take out debt. The battle for AI is increasingly forcing hyperscalers to sacrifice shareholder payments and equity for datacenter Capex. The Mag 7 is down -6.7% year to date.

The picture under the surface in 2026 is of all out battle. Many stocks have been hit hard and many others have made great progress. The S&P 500 fails to tell the whole story as it remains unbothered near all time highs.

Value stocks face an entirely different reality than tech stocks, and stand among the early victors. Many sell tangible goods. Very few are threatened by innovative growth. Most feel so unthreatened that they can entirely resist the slippery Capex slope. And they have cheaper multiples?

We can see these tailwinds from a macroeconomic lens too.

Many of these value stocks fall into the “cyclical” variety, meaning they are much more sensitive to financial conditions. I wrote this piece last September about how financial conditions are easing after a few restrictive years. Cyclical stocks now have more tailwinds from friendly financing.

Value stocks also outperform during periods of higher growth.

Growth drives yields higher and prices lower. Yes, that seems like a paradox, but Growth = Disruption and Disruption = Lost Market Share. Value stocks already have attractive yields so they experience less price damage during these moments of economic acceleration.

And so suddenly the ugly sweater has a feeling of safety to it. The skirmish in tech is heating up right as the macroeconomic environment eases for cyclical value stocks.

I still expect a business friendly environment in 2026, but there are both more winners and more losers so far than in recent years. Index funds are at risk of underperformance, for the first time in many years, because of how little non-tech diversification the most popular options offer.

There will come a time when active investing far outpaces passive investing for five or more years, and I wonder if we’re experiencing such a pivotal moment. I believe Artificial Alpha’s Large-Cap Value Portfolio is well-positioned to make these adjustments if they prove valuable, as they have so far this year.