Investing Through an Inflation Shock

And Finding Proof For Patience

Like everyone else, I find myself preparing for an inflationary environment after the U.S. invasion of Iran a few weeks ago. This is a frightening prospect for risk takers.

The Setup

The biggest economic risk caused by the war is the closing of the Strait of Hormuz and its effect on oil prices. Here are oil tanker crossings through the strait, courtesy of Joe Weisenthal.

And here is Oil’s reaction to these Middle East developments.

Since oil remains a key input to many economic activities, its price also remains a key driver of inflation.

Known Unknowns

Before I dive into some historical comparisons, I do have a few key considerations that remain unknowns.

First, the U.S. is a net exporter of oil. This was not the case during past inflationary shocks. The U.S. has historically been a net importer of oil and price spikes exacerbated inflationary shocks as opposed to damping them. We don’t know how oil prices will impact the U.S. economy this time.

Second, we know that geopolitical events average out to having almost no signal on market prices. What matters are outcomes and not the conflict itself. We do not know the outcome of this war yet.

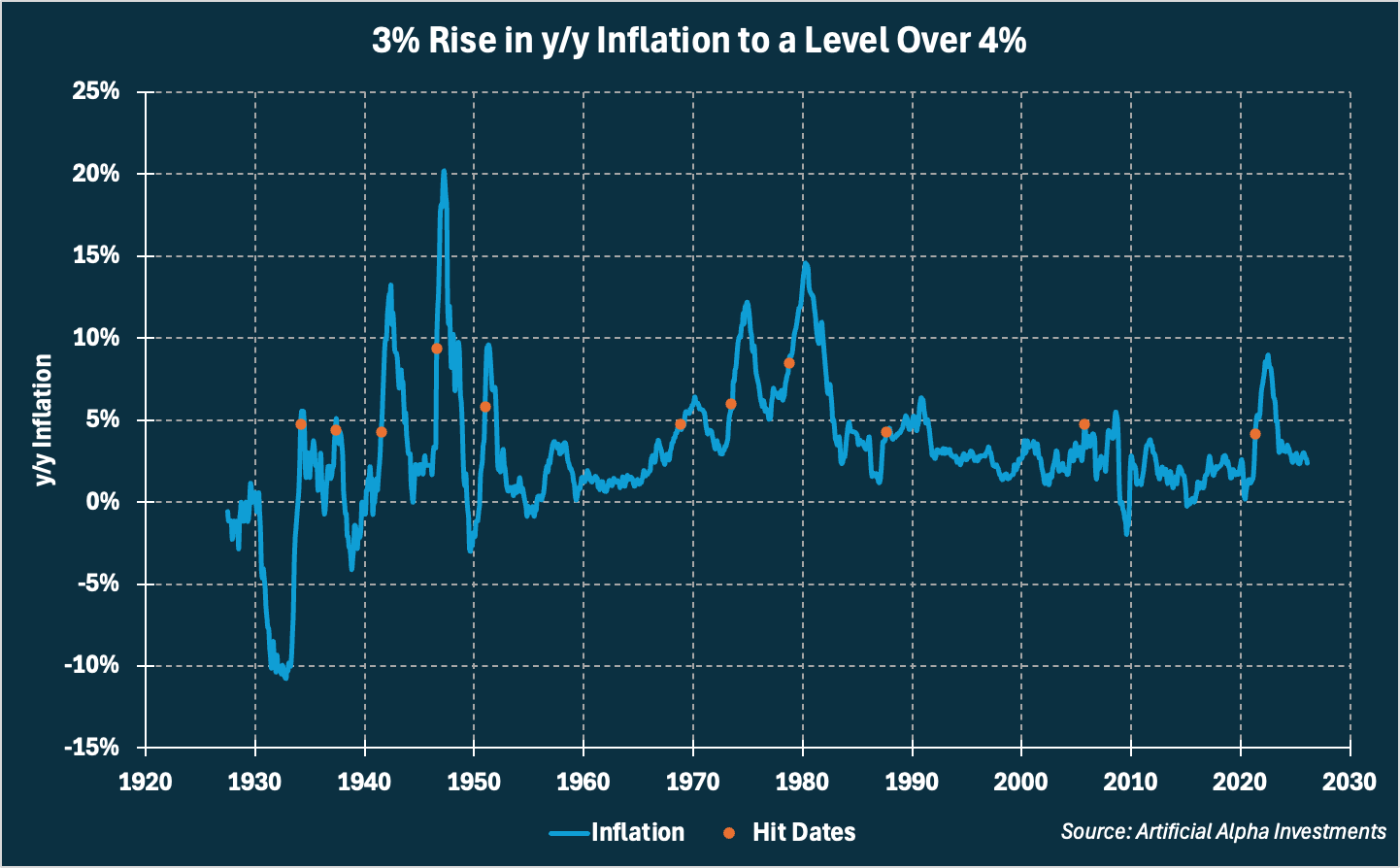

A Sample of Inflationary Shocks

To study how investors can plan with these unknowns in mind, I put together a sample of inflationary shocks. These are months where y/y inflation had risen more than 3% off its lows and to a level over 4%. These are confirmed moments of significant price acceleration.

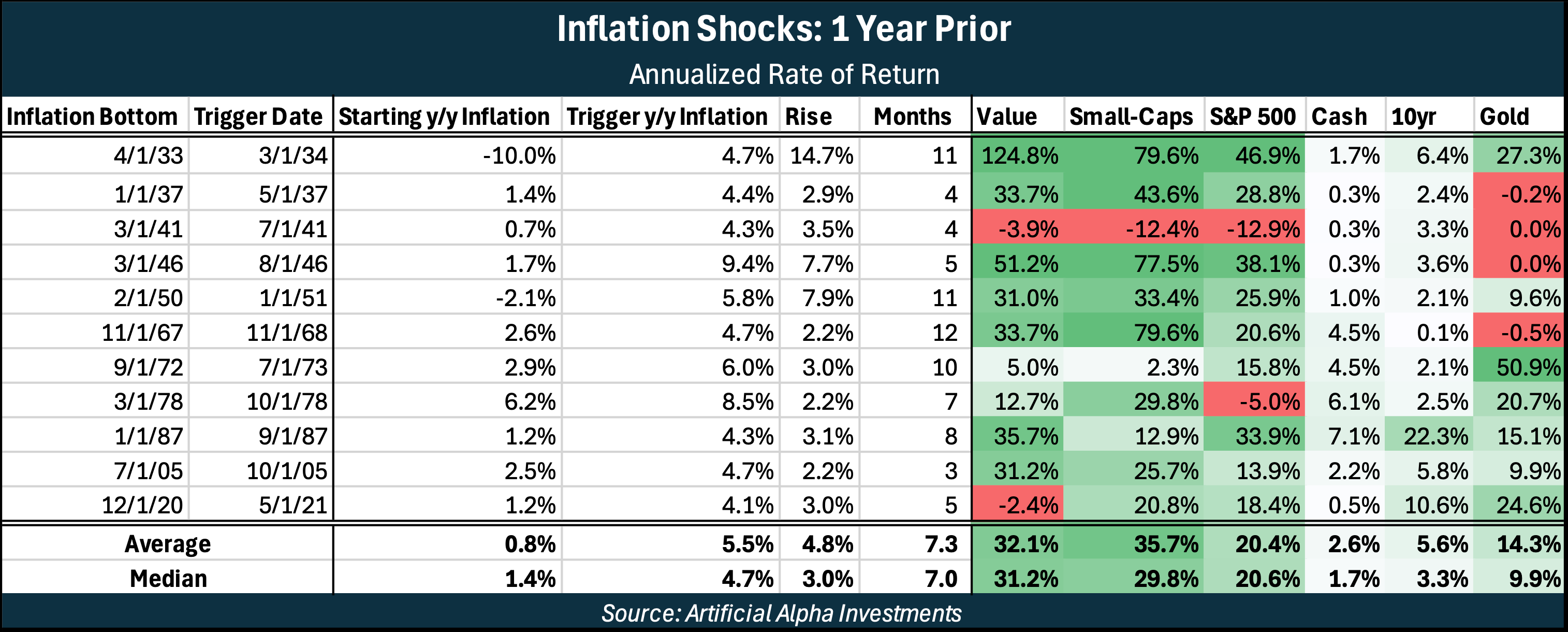

The market does not react in advance to inflationary catalysts. Below are the market returns for a few asset classes in the year prior to inflation bottoming and the moment of the catalyst. These periods of disinflation are amazing environments for financial assets.

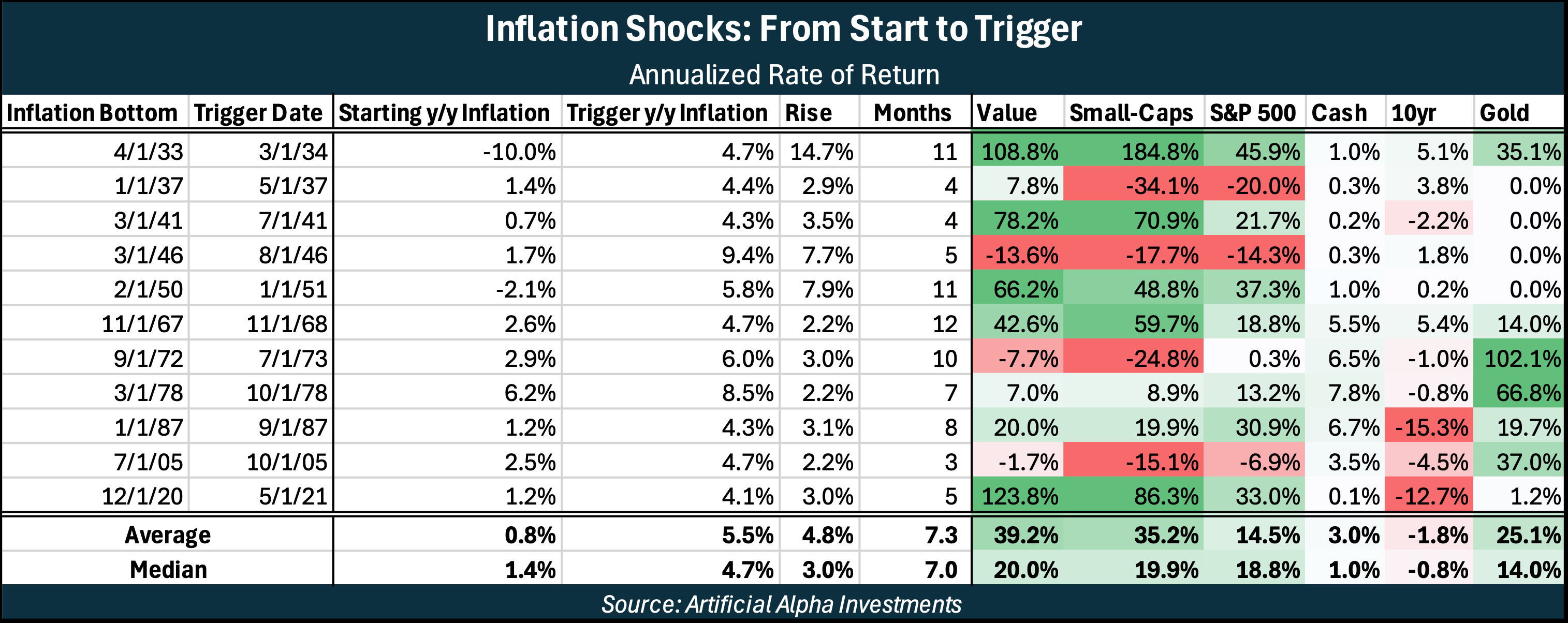

Then, an inflationary catalyst appears and inflation rises to an uncomfortable level above 4%. We can tell that these were strong inflationary events because inflation didn’t retreat for a single month in this whole sample. On average, it took 7 months to go from catalyst at inflation bottom to sample trigger above 4%. This is a long process!

During these runs in inflation, average returns were still great (outside of bonds) but now with a ton of variance and bimodal outcomes.

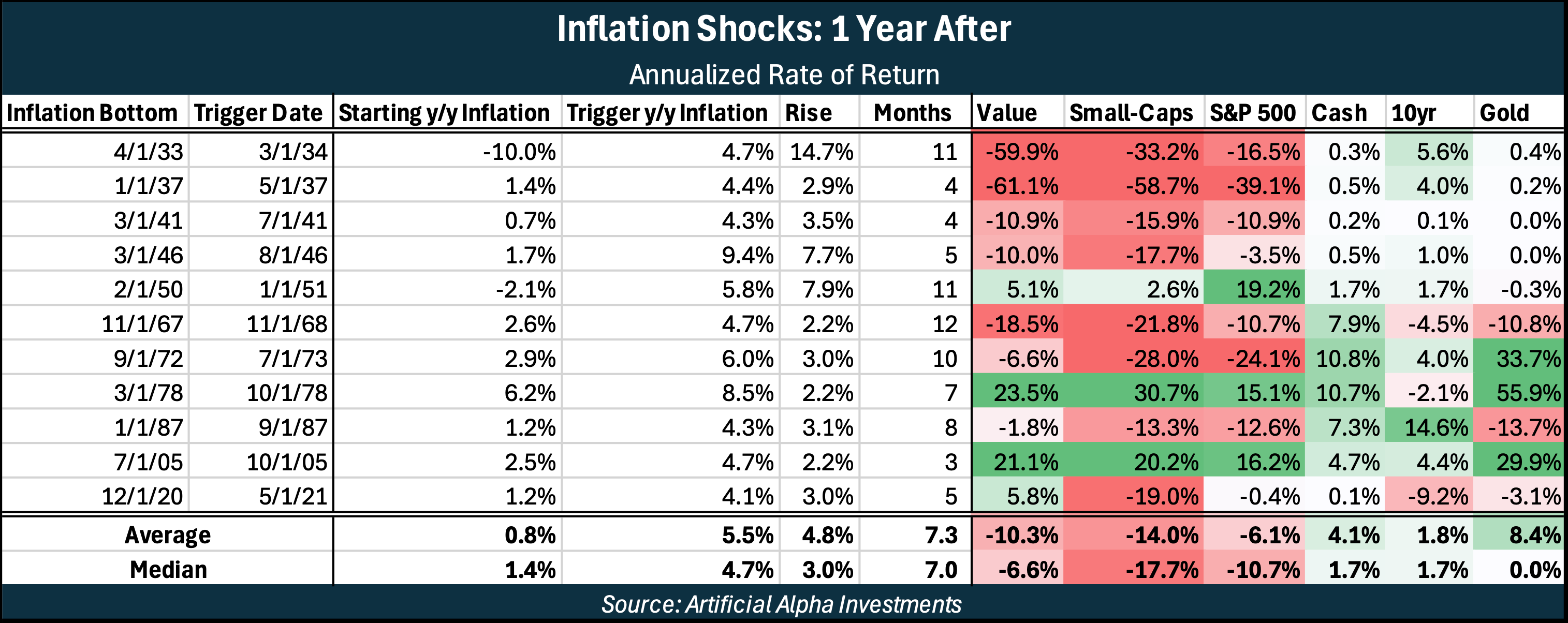

It is only in the year after complete confirmation by government data that the market shows signs of stress. And the stress is real. This is about as bad a sample for stocks as I can find.

Staying Patient

These data are kind of insane. Huge returns followed by big drawdowns. However, keep in mind that these comparisons are still just a risk of this war and not a sure outcome. Additionally, it actually isn’t apparent that investors should panic quite yet. Maybe quite the opposite actually.

I don’t know your personality as an investor, so I can’t give you specific advice. But here are two lines of thought for the given moment that might suit two generic types of investors.

You’re an active investor and you want to hedge inflation risks. History says that a melt-up in stocks is just as common as a crash until inflation gets baked into the data. If your goal of active investing is to reduce portfolio volatility, gold has been a much better hedge than bonds outside of gold standard environments.

You’re a passive investor and you never want to alter your stock portfolio but you’re uncomfortable by these risks posed by the war. Consider that we tend to leave gains on the table during these moments of uncertainty, not losses. Volatility during these moments is huge but overall outcomes are average to above average. As passive investors should ideally set out to do, stay the course!

Conclusion

I’ve been writing a lot in the past few years about taking more stock diversification than the S&P 500 and when to use gold and other commodities as a hedge against risk. I don’t think these geopolitical developments diminish those ideas, in fact I believe they reinforce them.