Hello, Inflation

A Note on Federal Reserve Interest Rate Policy

This is primarily an economics letter, not an investment or markets letter. Knowing my audience, this one probably isn’t your thing.

Also, I’m not going to say the b***le word in this forum but you can follow me on X or grab a drink with me IRL for a debate on that. I want to clear my thoughts on interest rates before I come to a hard stance on the stock market.

Introducing: The Federal Reserve

Prior to the Fed, the banks that bought Treasuries were profit making institutions. They amplified the business cycle and, because they were so involved in Treasury markets, frequently destabilized the money and banking markets the government relied on. The Fed was created in 1913 to stabilize a debt market that lacked sufficient stabilizing incentives.

The Fed’s goal of market stability is really hard to interpret and measure, however. That is why Congress wrote more explicit goals into law in 1977, for the Fed to “promote maximum employment and stable prices.”

The Fed now sets short-term interest rates instead of the market. In consideration of their mandate, the Fed should keep interest rates low enough to promote investment and employment and high enough to suppress inflation and business instability.

You will notice that this framing pits the Fed’s goals against each other. Any call for the Fed to fight inflation is also an implicit call for the Fed to sacrifice employment, and vice versa. I believe an optimal rate of interest exists that optimizes for holistic outcomes but that doesn’t mean the Fed’s set of possibilities is always attractive.

The Federal Reserve Reaction Function

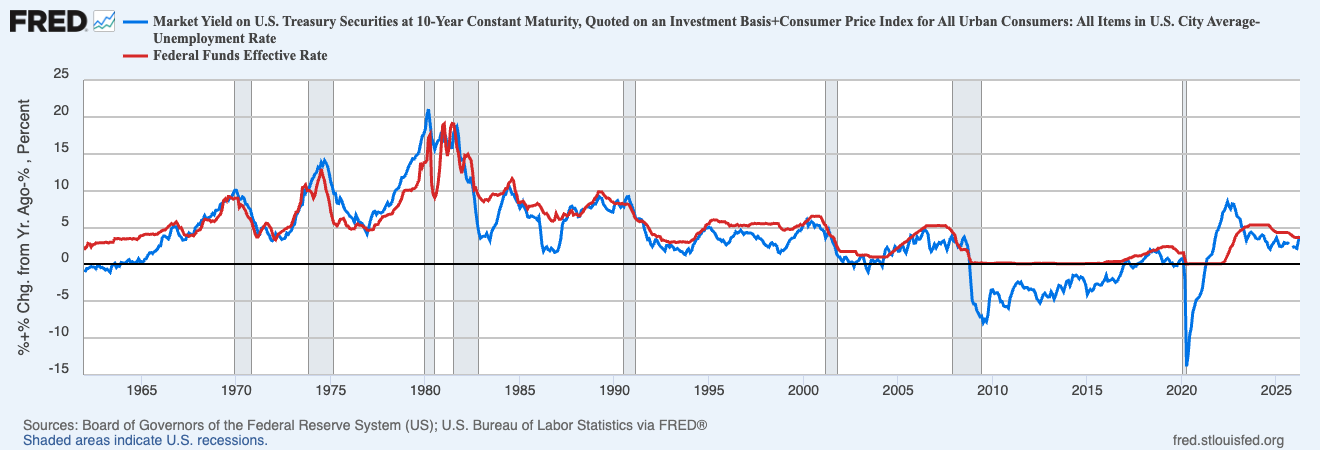

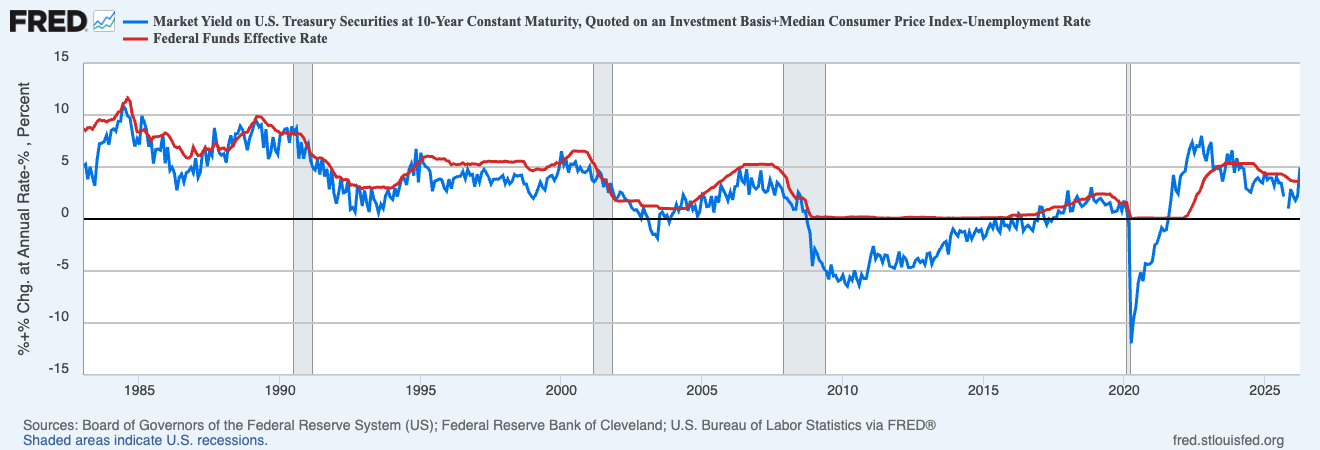

The following chart makes a ton of sense in light of the Fed’s implied capacity to affect balance. The red line is the interest rate set by the Fed. The blue line = 10yr + Inflation - Unemployment.

The 10yr Treasury yield is an estimate of long-term growth. The Fed primarily sets their rate based on the 10yr’s market-based growth estimate.

Then, the Fed adjusts their rate higher or lower based on the imbalance between inflation and unemployment. Higher inflation and lower unemployment means the Fed needs rates higher than long-term growth to bring inflation and unemployment back in balance.

This chart is a simplified visualization of the Fed’s decision making process. But it shows that the Fed roughly sets policy based on long-term growth expectations plus any short-term economic imbalances between inflation and unemployment.

“Watch what they do not what they say.” The Fed interprets their mandate as a chase for balance and they have historically set interest rates in line with this belief. The Fed’s 2% inflation target overly simplifies their mandate and does not act as a goal they should expect to achieve in all economies.

A 2026 Inflation Shock

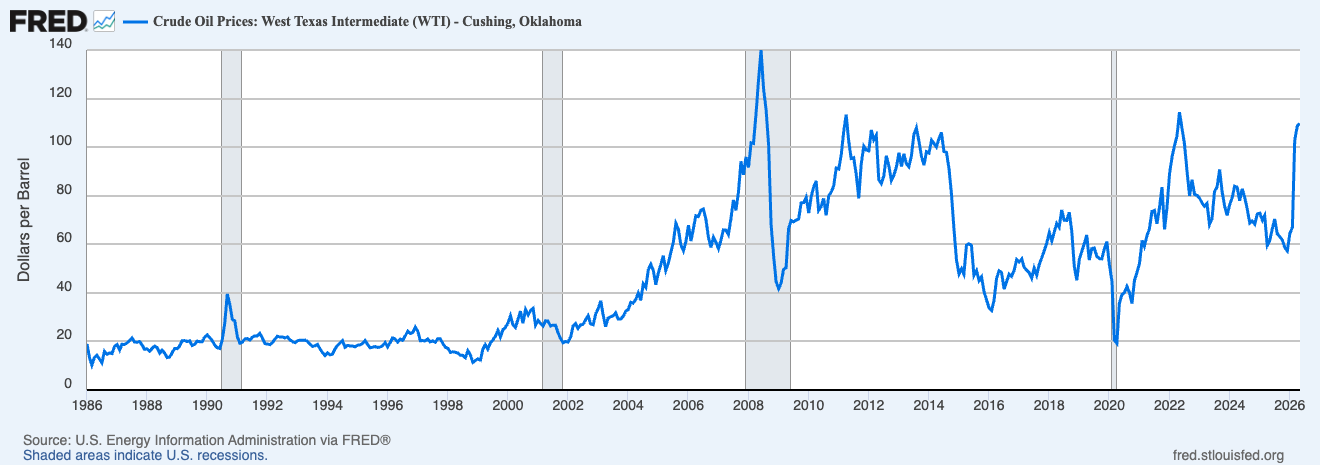

This year is full of inflationary shocks, primary of which comes via the war in Iran.

Iran’s strategy of blocking oil exports through the Strait of Hormuz and America’s strategy of reinforcing that blockage have sent oil prices much higher. Oil prices are still a key input to most business activities.

And America’s heavy use of military assets in Iran pushes the government to further debase the dollar via military government expenditures.

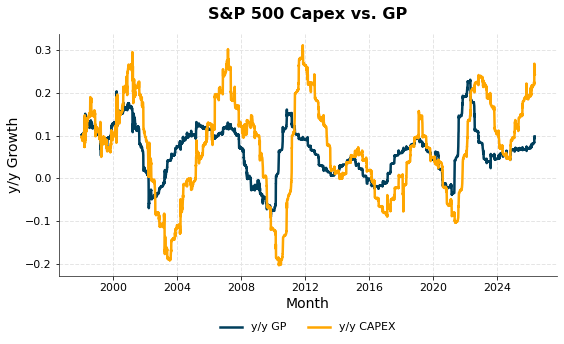

On top of a war-induced supply shock and a military investment boom, private industry is piling money into AI investments.

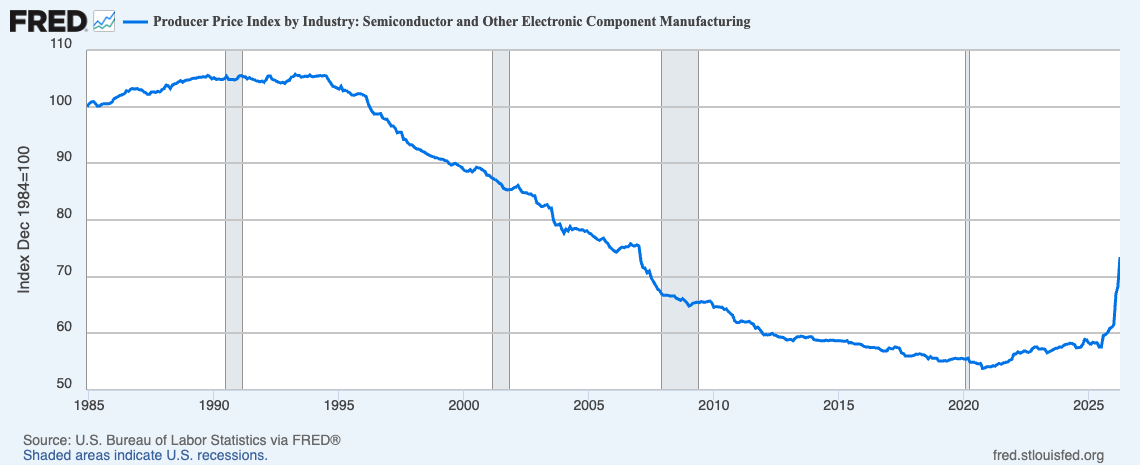

All this investment, especially capex that is being funded by borrowing as opposed to gross profits, is slamming into bottlenecks up the supply chain. Not just the oil and gas and plastics and fertilizers being blocked from the Persian Gulf, but also semi-conductors with tight supplies and long lead times.

Memory related semiconductor stocks are up 60.7% over just the past month.

Unfortunately, this stock market phenomenon is largely indicative of higher prices in the AI investment race. S&P 500 semiconductor capex is only up 1% y/y while gross profits are up 44% y/y. Many other supply chain industries look the same. The AI supply chain wasn’t ready for this much investment demand so it dramatically raised prices.

We can now see government data starting to get a read on semiconductor inflation.

A ton of money is being invested by both government and private industry while supply chains are either reeling or flat footed. Demand is up and supply is flat or down.

A 2026 Policy Shock?

This all adds up to an inflation shock that changes the rate needed to balance the economy.

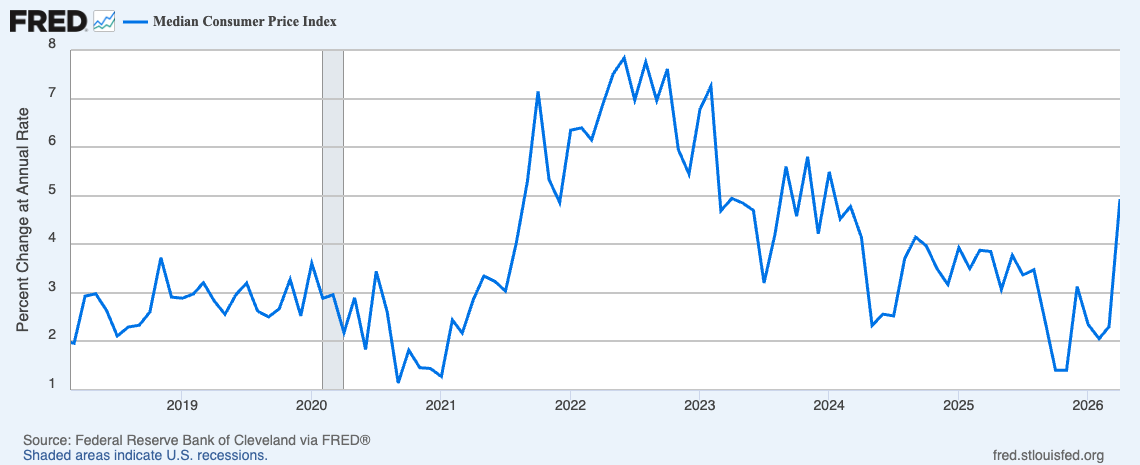

Inflation officially arrived to government data in April. The deflationary impacts of AI on services inflation are not nearly enough to counteract the inflationary impacts of war and supply chain frictions on goods inflation. Median CPI jumped from 2.3% m/m in March to 4.9% m/m in April and I expect it to continue rising.

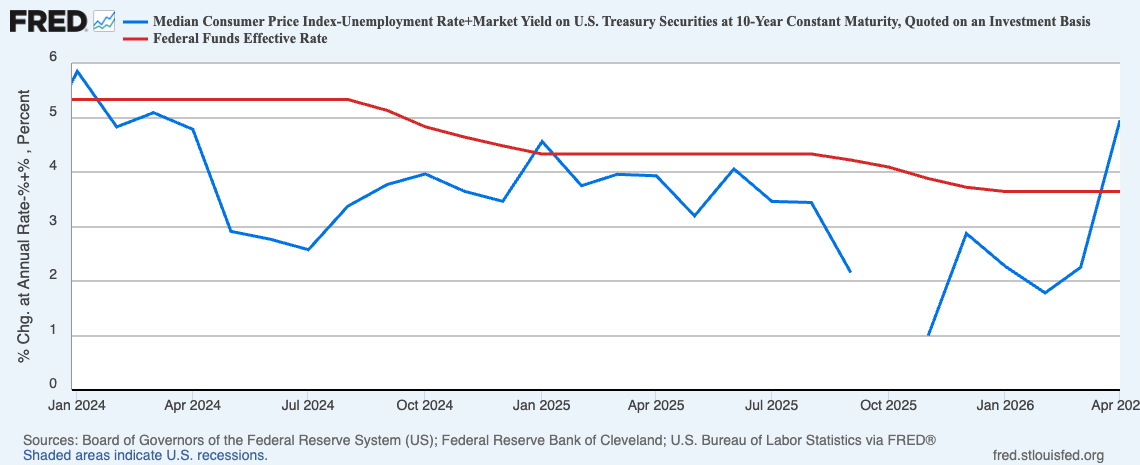

Below is the same policy estimate chart from before but I substituted m/m median inflation in place of y/y inflation to get a higher frequency look of the latest data.

This simple calculation suggests that a strong-willed Fed would raise rates after a few more months of hot inflation.

Conclusion

The Fed was created to disincentivize lending in a timely manner during inflationary booms so that we can avoid deflationary busts. The war in Iran is pushing up consumer prices and the AI supply chain is proving far from frictionless. Newly realized inflation data will put more and more pressure on the Fed to hike so that only high quality investments continue to get funded. Of course, if you’re familiar with the Fed’s current struggle for independence, higher rates are not a sure thing.