Investment Account Types

With Timing and Application Considerations

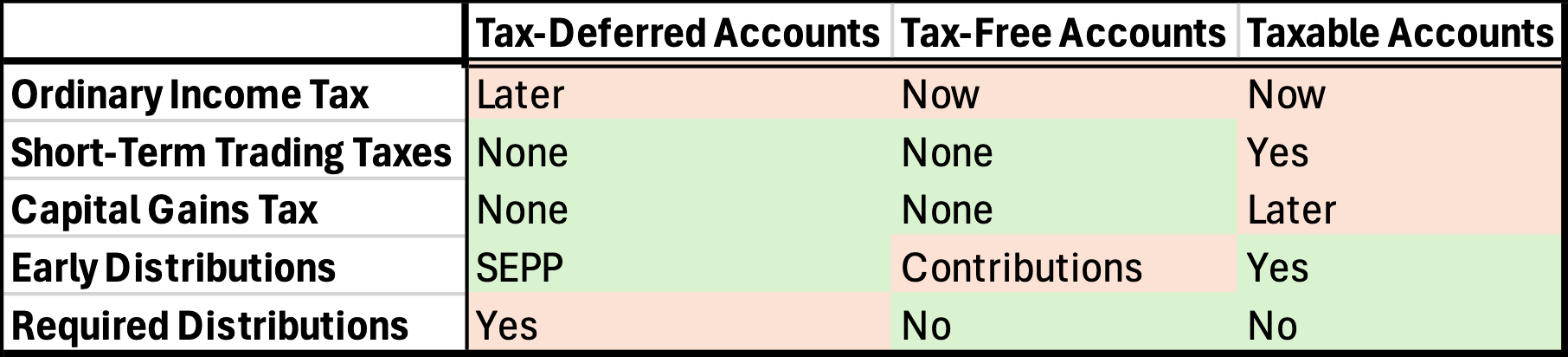

This is a tax, distribution, and application summary of the 3 investment account types that I find most important for retirement planning. Please pay particular attention to the characteristics and strengths of Tax-Deferred Accounts. I find Tax-Deferred Accounts uniquely useful despite going more and more unemployed by bigger advisors.

Taxes

Tax‑Deferred Accounts (Traditional)

Income: Untaxed on Traditional 401(k)s and untaxed on Traditional IRAs depending on coverage and gross income

Short-Term Capital Gains: Untaxed

Long-Term Capital Gains: Untaxed

Distributions: Ordinary Income Rate

Tax‑Free Accounts (Roth)

Income: Ordinary Income Rate

Short-Term Capital Gains: Untaxed

Long-Term Capital Gains: Untaxed

Distributions: Untaxed

Taxable Accounts

Income: Ordinary Income Rate

Short-Term Capital Gains: Ordinary Income Rate

Long-Term Capital Gains: Long-Term Capital Gains Rate

Distributions: N/A

A Brief Note on Conversions…

401(k)s have high contribution limits and powerful tax deductions, but investments and platforms are often limited by the plan provider and mutual fund fees can be much higher than ETF fees.

Consider rolling 401(k)s into a matching IRA after a qualifying event (like leaving an employer) for investment, advisor, and fee flexibility. A Traditional 401(k) can be rolled into a Traditional IRA and a Roth 401(k) can be rolled into a Roth IRA.

Further, because intra-IRA sales are untaxed, IRA assets are most suitable for active strategies like Artificial Alpha’s Large-Cap Value Portfolio.

Distributions

Tax‑Deferred Accounts (Traditional)

Unpenalized Early Distributions: Substantially Equal Periodic Payment plans or a Roth Conversion Ladder

Unrestricted Distribution Age: 59.5

Required Minimum Distributions: 73

Tax‑Free Accounts (Roth)

Unpenalized Early Distributions: Roth IRA Contributions, among other circumstances

Unrestricted Distribution Age: 59.5

Required Minimum Distributions: N/A

Taxable Accounts

Unpenalized Early Distributions: N/A

Unrestricted Distribution Age: N/A

Required Minimum Distributions: N/A

Optimal Applications

I would color the strengths/weaknesses heat map for each account type like this.

Traditional Retirement Accounts cover early retirement and base-level spending.

Ideally, you should contribute to a Traditional Retirement Account when you’re middle-aged and contributions are deducted from a high tax bracket. It is not desirable to over-contribute to a Traditional Retirement Account because required minimum distributions in retirement could subject your income to a higher tax bracket.

The superpower of a Traditional Retirement Account is that it combines tax savings and early distribution. An early retirement can be funded by setting up a SEPP plan (or a Roth Conversion Ladder) and primarily living off Traditional Retirement Account distributions. Technically you can withdraw Roth IRA contributions early without penalty, but those sums are not great enough for an extended early retirement.

Roth Retirement Accounts cover one-offs, gaps, and late retirement.

Ideally, you should contribute to a Roth Retirement Account when you’re young so that distributions can go untaxed later in life while in a higher tax bracket. It is somewhat desirable to over-contribute to a Roth Retirement Account because there are no required minimum distributions in retirement and distributions by heirs remain untaxed.

The superpower of a Roth Retirement Account is that all taxes are out of the way after contribution and Roth IRA contributions can be distributed early without penalty. This makes Roth distributions perfect for emergency expenses during early retirement, excess spending during retirement, and base-level spending when Traditional distributions run dry in late retirement.

Taxable Brokerage Accounts cover big purchases and miscalculations at any time.

Taxable Brokerage Accounts are where excess savings go. It is desirable to over-contribute to a Taxable Brokerage Account because the money inherits no limitations.

The superpower of a Taxable Brokerage Account is that it maintains maximum flexibility. Technically, you could perfectly fund a tax-efficient early retirement with some combination of Traditional and Roth Retirement Accounts. But any error in planning or surplus contributions imposes limitations on those contributions that might dwarf the impact of any tax savings. Contributing to a Taxable Brokerage Account lets you figure out the details later.

Conclusion

I especially wanted to write this letter because SEPP plans (or Roth Conversion Ladders) are not widely utilized. It is exceedingly popular to forgo Tax-Deferred Accounts entirely, but I think that is a mistake if early distributions are even remotely in the cards. Tax-Deferred Accounts are the only ones that combine tax savings and considerable early distributions.

On top of application differences, I also find value in tax diversification and tax smoothing. These benefits are improved by contributing to both Traditional and Roth accounts.

Each account type has its own unique timing, application, and tax implications. Very generally, I might argue that each application requires similarly sized funds. Clearly there is more precise, client-specific planning to do, but one rule of thumb might be to end up with 1/3 of assets in each account.