Stock Market Concentration (pt. 3)

Parts 1 and 2 established that today’s stock market is more concentrated than all but two months from the prior 100 years. Additionally, this market concentration is not necessarily warranted, considering the large-cap vs. mid-cap valuation divide is as large as during the tech bubble in 2000.

Is it time to diversify into mid-caps and small-caps? This analysis continues to attack that question by providing some historical context for current levels of concentration and valuation.

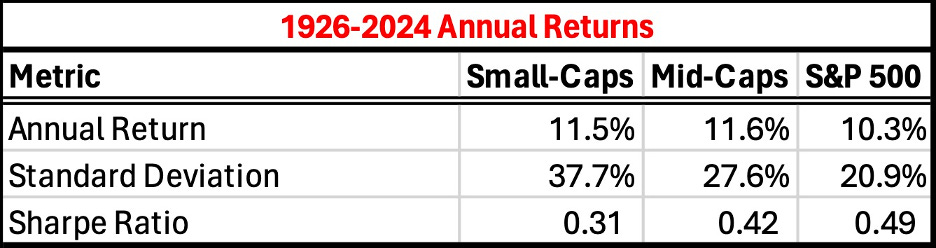

On average, mid-caps and small-caps carry no magical properties.

The average annual return of mid-caps and small-caps has been greater than large-caps, but those higher returns have been paid for via much higher volatility. The Sharpe Ratio, which compares returns to volatility by dividing the average over the standard deviation, suggests that large-caps have provided higher quality returns over the past century.

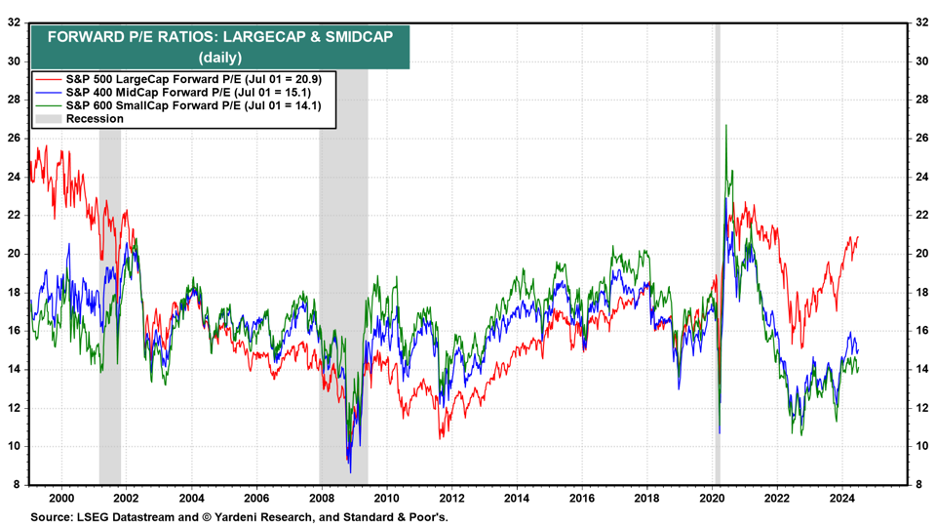

Comparable returns explain why neither large-caps, mid-caps, nor small-caps have a historical claim to higher valuations. Now, though, the large-cap valuation divide is as large as during the tech bubble in 2000.

And the difference between a 21 P/E for large-caps and a 14 P/E for small-caps is mathematically significant. If small-caps were to catch up to a 21 P/E over the next 5 years via price growth alone, they would enjoy an additional 8.4% annual advantage during that time. If mid-caps were to catch up to a 21 P/E over the next 5 years, they would enjoy an additional 7.0% annual advantage during that time.

This calculation is too simple since it ignores the accuracy of earnings expectations and each index’s ensuing earnings growth. Valuations not only converged between 2000 and 2005, but large-cap earnings fell far short of their unrealistic expectations. Mid-caps ended up outperforming by 10.1% and small-caps by 15.3% per year between 2000 and 2005.

The complexity of using valuations to set measurable forward expectations is why I prefer to find comparable historical events and measure ensuing results instead.

There have only been three other periods since 1926 when the largest 10% of stocks carried a market share of 72% or more. What precedent does history provide for these extremes of large-cap concentration

The following table groups our sample into three periods of high concentration. Returns are for equal investments made during the indicated period.

On average, mid-caps and small-caps outperformed the S&P 500 by 18.7% and 12.2% per year for 5 years when concentration in large-caps was as extreme as it is today. Mid-caps and small-caps even did well during the ‘00s tech bust.

The next two charts show the ratio of mid-cap and small-cap returns to large-cap returns. Mid-caps and small-caps were outperforming large-caps in these charts when the ratio was increasing, and vice versa. The months in which the largest 10% of stocks had a market share above 72% and were therefore included in our sample are highlighted in red.

In the same way that valuations correct over long periods of time, mid-caps and small-caps enjoyed 5+ years of tailwinds after these concentration extremes. When/if a mid-cap and small-cap theme emerges, we should expect it to be a long-term opportunity.

Because the timeframe on this idea is decently long, I am not personally rushing to act in a big way until I get some sort of confirmation. I made a small investment in mid-caps and small-caps last week, but far less than I plan on holding if more investors start sharing my view of the future.

Bottom line from parts 1, 2, and 3.

Large-cap valuations are stretched, and history shows that eventual mid-cap and small-cap outperformance could be even greater than those valuation differences suggest.

I’m intentionally splitting this into parts because FOMO is not super helpful here due to the long-term nature of this idea. In the coming week or two I will write about my favorite ETFs for investing in mid-caps and small-caps and context for a reasonable allocation.

Feel free to reach out with questions. I’m happy to discuss some of the countless personal considerations that cannot be tackled in these letters.