Stock Market Concentration (pt. 2)

I have predominantly allocated my long-term indexed investments toward the S&P 500 for years now. Increasingly, however, I’m worried about how little diversification I’m getting from an S&P 500 index fund.

Additionally, I am worried about the effect that S&P 500 valuations will have on my investments over the coming decade. Are there pockets of the market with better prices?

I shared this chart of S&P 500 concentration within the largest 5 holdings in March. Since then, the largest stocks have continued to outperform. Four months later, those 5 companies now claim 28.6% of the S&P 500 market share.

Unordinary stock market concentration extends beyond the S&P 500 to the entire stock market itself. The next chart calculates the market share of the largest 10% of stocks as a percentage of the entire stock market.

Large-caps, like those stocks in the S&P 500, had a market share of 74.7% at the end of May 2024.

This increased concentration has come at the detriment of small-caps and mid-caps (defined going forward as the smallest 30% of stocks and the middle 40% of stocks). If you’re an active investor like me, it’s been a hard year and a half to compare yourself in any way to the largest 5 stocks.

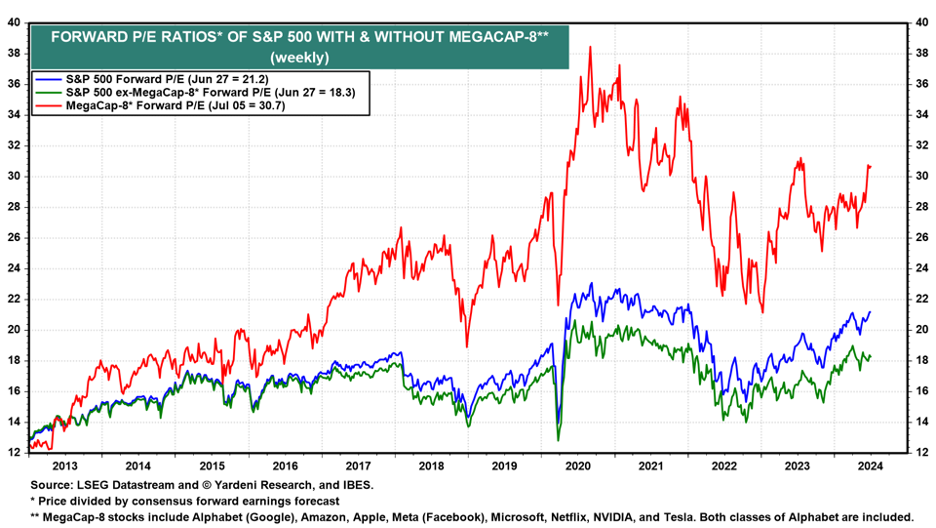

Not only do the largest companies claim a record share of market cap, but they are also increasingly expensive in comparison to their earnings. Google, Amazon, Apple, Facebook, Microsoft, Netflix, NVIDIA, and Tesla make up 31.0% of the S&P 500 and combine for a 30.7 P/E ratio on next year’s projected earnings.

The rest of the S&P 500 carries an 18.3 P/E on next year’s projected earnings.

Looking past the large-caps in the S&P 500, mid-caps and small-caps carry P/E ratios of 14.8x and 13.9x respectively.

I analyzed the equal weight S&P 500 in my March letter as a potential alternative to the S&P 500, but these market-wide concentration and valuation extremes have me wondering if I should be looking even further towards mid-caps and small-caps.

Market concentration and valuation divergences are topics that will be given a lot of attention in the coming months. I’m already planning on writing about historical analogs, back of the napkin valuation consequences, relevant ETFs, and timeframe considerations in upcoming letters.