Rent vs. Buy

Napkin math on housing decisions

The tradeoffs of owning vs. renting a home are extremely complicated. I made this excel doc to simplify the decision from a financial perspective.

The “Inputs” tab has 14 variables that need to be filled in to estimate the cost/profit of each choice.

B3:B5 are the growth rates of the home and an alternate investment portfolio. I would recommend using the long-term growth rates provided.

B6:B12 are the costs associated with owning the home. I entered nationwide averages for these fields but they vary wildly by state. I would recommend editing these inputs for a more accurate calculation.

B13:B16 are inputs for the home and mortgage. I found a home here in Colorado for this example.

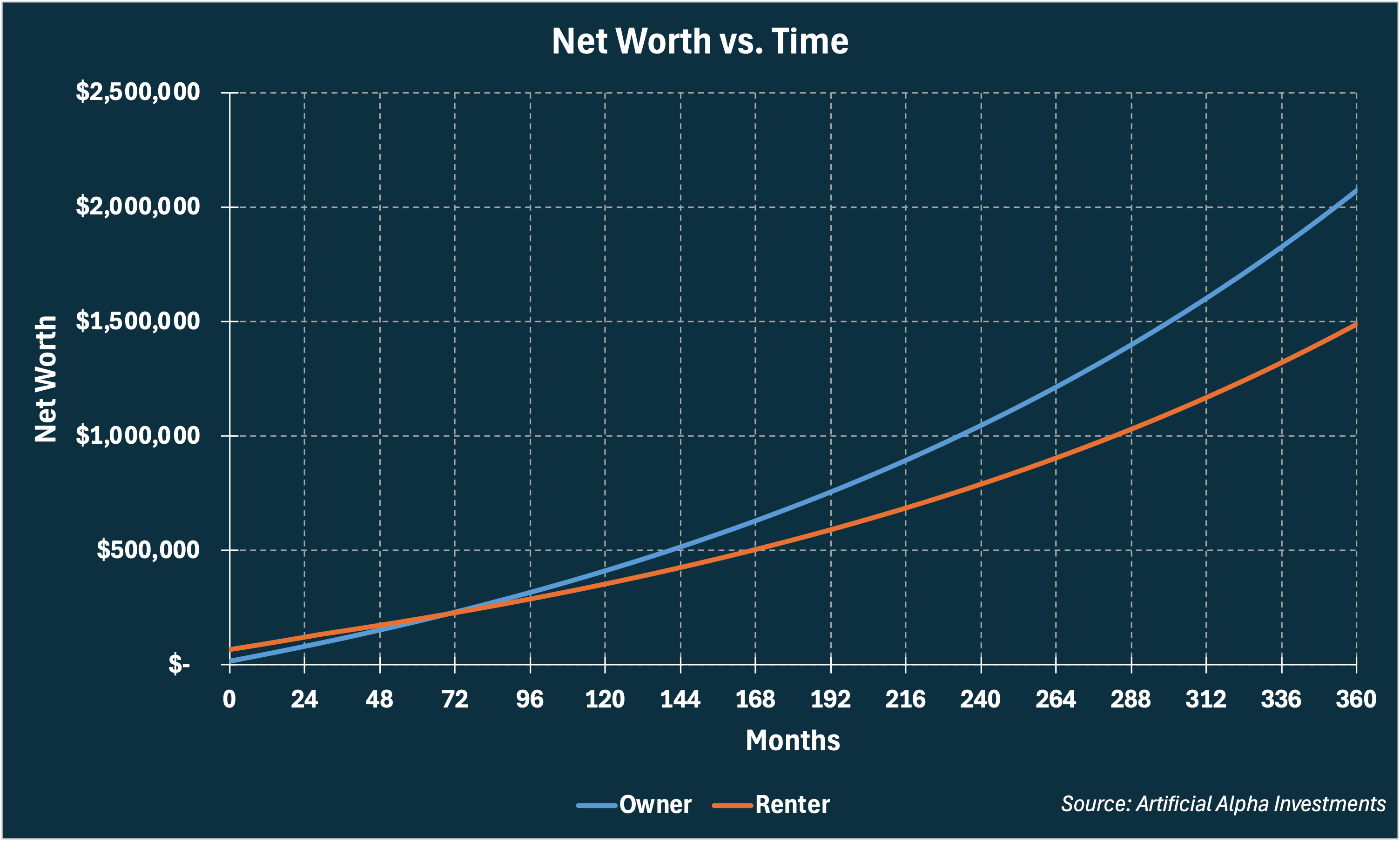

The “Monthly Balance Sheet” tab calculates the net worth for the owner and the renter across all 360 months of a 30 year mortgage, assuming the renter invests their excess savings into a diverse portfolio of stocks, bonds, and gold.

Buy to Stay, Rent to Move

The owner loses fees on their transaction(s), but then generally sees their net worth grow faster over time after that. This means they always start lower and usually end higher in the race for wealth.

The break-even point, at which both owner and renter have the same net worth, and where these lines cross, is calculated in B18. Sometimes a poorly priced market will not see these lines cross at all. That a breakeven point exists at all is dependent on a fairly priced rental market.

The example I have pre-populated illustrates the general calculus, simplified into a one-variable rule. Buy a house if you plan on staying in one place for longer than 5-7 years. Rent if you don’t. The default values are from the first rental example I found on Zillow in Denver. Most middle-class housing markets are priced for a similar tradeoff!

Homeownership Is a Savings Account

Next turn to F2:F4, where I subtract the home owner’s total payments from their final net worth. I am going to round the Profit calculation up to $0 to simplify my claim, which is that the average home owner comes out even in the end. Their savings do not depreciate. Neither do their savings compound. Putting money into your house resembles depositing money into a savings account (with much more variance).

This means that buying a bigger house is just like putting more money into a savings account. The opportunity cost of buying a bigger house is making actual investments with the difference in cost.

Conclusion

Wealth isn’t made by consuming housing, especially as a renter.

Please use this tool to do napkin math on houses in your area. I have friends whose rent is so cheap that it makes very little financial sense for them to buy!

And of course, there are far more variables than the financial ones that go into any home buying decision.